Investment Boost

What is Investment Boost?

Investment Boost is a new tax incentive for New Zealand businesses to invest in productive assets like machinery, tools and equipment. Businesses can deduct 20 per cent of the new asset’s value from that year’s taxable income, on top of normal depreciation. The deduction applies to new assets purchased from today, 22 May 2025.

Why is the Government introducing Investment Boost?

Investment Boost improves the cashflow from new investments, meaning more investment opportunities become financially viable and therefore take place. Business investment raises the productivity of workers, lifts incomes and drives long-term economic growth. By increasing the stock of capital in New Zealand, Investment Boost is expected to lift GDP by 1 per cent and wages by 1.5 per cent over the next 20 years, with half these gains in the next five years.

How does it work?

Businesses can deduct 20% of the cost of new assets in the year that they purchase the asset.

The deduction applies to new assets purchased from 22 May 2025.

You can claim both the investment boost and the standard depreciation deduction in the year you purchase the asset.

Investment Boost Criteria

The asset must be:

New or new to New Zealand

Available for business use on or after 22 May 2025

Depreciable for tax purposes

Assets the Investment Boost Does Not Cover

Assets that have previously been used in New Zealand (secondhand assets)

Land (although land improvements may be eligible)

Assets that will be held as trading stock

Residential Buildings (dwellings)

Fixed-life intangible assets (such as patents)

Assets that are fully expensed under other rules (such as assets under $1,000)

Most buildings used to provide accommodation (except for hotels, hospitals and rest homes)

Assets Purchased from Overseas

Investment boost can be claimed on both new and second-hand assets if they are purchased from overseas on or after 22 May 2025.

Investment Boost – Not Compulsory

The investment boost claim is not compulsory. It is optional to claim the deduction for new assets. This may be preferable for businesses to claim the standard depreciation only if the business expects to make losses in the early years, such as start ups

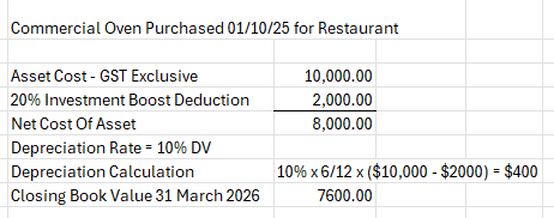

Depreciation Calculation

The base from which standard depreciation is calculated is reduced by the amount of the investment boost deduction. In the year that you purchase the asset you can claim:

20% of the cost of the asset plus

The amount of the usual depreciation deduction that would otherwise apply but calculated as if the cost of the asset was reduced by 20%

Example:

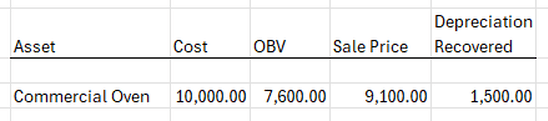

Asset Sale & Depreciation Recovered

Just like depreciation, some or all of the investment boost deduction may be recoverable if the asset is disposed of and the consideration is more than the assets book value.

Assets Partly Used in Business

You can claim investment boost on the business-use portion of the asset. You cannot claim investment boost for an asset to the extent it is used for private purposes

New Commercial Buildings

New commercial and industrial buildings are eligible for investment boost (even though the depreciation rate on buildings is 0)

Residential buildings are not eligible for investment boost.

Construction Project

If a taxpayer started a construction project on a commercial or industrial building before 22 May 2025, the asset may be eligible for investment boost. The asset needs to be used or available for use for the first time on or after 22 May 2025.

Capital Improvements on Existing Commercial Buildings

The investment boost deduction can be claimed on an asset owned by the taxpayer if the asset is:

Depreciable property for which the taxpayer has a depreciation loss, including a zero amount of depreciation loss (for example, some commercial buildings)

An improvement to an asset

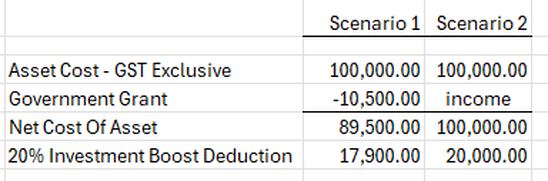

Government Grants & Cost of Asset After Investment Boost

Section DF 1 (3) applies to Government grants applied to the purchase of an asset

The taxpayer can choose to either:

Claim 20% on the net cost of the asset after the credit for the Government grant or

Claim 20% of the asset cost as an investment boost deduction and declare the Government grant as taxable income

We await some additional detail in regard to the practicalities of the Investment Boost application and there are always some scenarios come up that new legislation did not account for in the initial drafting.

Additional information can be found by following the following link: